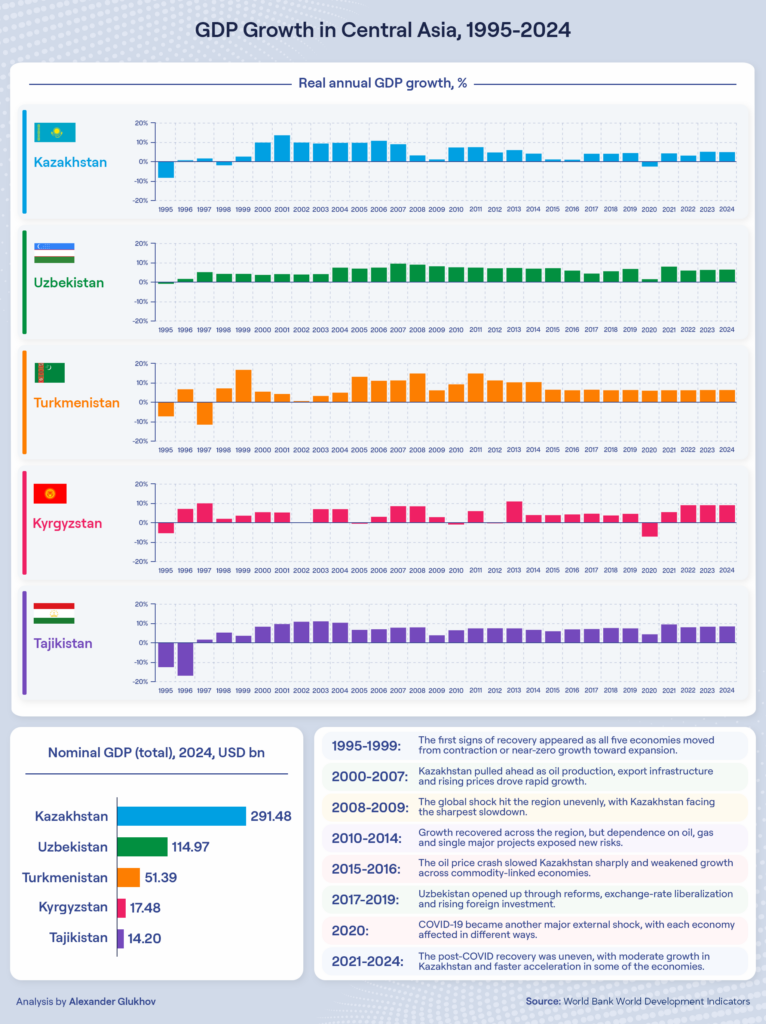

30 Years of GDP Growth in Central Asia

Between 1995 and 2024, the economies of Central Asia emerged from the post-Soviet collapse, went through a commodity boom, the global financial crisis, the oil price crash, COVID-19, and a new cycle of regional growth.

1995–1999: First signs of recovery

In 1995, all five economies were either still contracting or only just beginning to recover. The deepest contraction was in Tajikistan: GDP fell by 12.4% in 1995 and by another 16.7% a year later. The downturn in Tajikistan went far beyond the general post-Soviet transition crisis. The civil war of 1992–1997 had devastated a significant part of the country’s industrial base.

Kazakhstan recorded a contraction of 8.2% in 1995. The country already had an oil base, but in the mid-1990s its export infrastructure had not yet been built. The CPC pipeline was still not in operation, and the privatization of the oil and gas sector was taking place amid institutional instability. Turkmenistan contracted by 7.2% in 1995. Gas was being produced, but debt disputes led Russia to close transit routes, effectively stopping exports. In 1997, Gazprom effectively blocked Turkmen gas transit to Europe amid pricing disputes and other countries’ inability to pay in cash, contributing to a sharp export decline and an 11.4% GDP contraction.

Uzbekistan looked more stable than its neighbors. After a relatively mild contraction of 0.9% in 1995, the economy returned to growth as early as 1996. Heavy state control over prices and foreign trade held back reform, but it also shielded the economy from more severe shocks. Kyrgyzstan, by contrast, moved through liberalization and paid for it with a deeper decline: GDP fell by 5.4% in 1995 before rebounding sharply to 9.9% growth in 1997, driven by a low base and the start of production at Kumtor.

By the late 1990s, all five economies were growing again. Much of it was still a recovery from the deep contraction of the first half of the decade, while sustainable economic models were only beginning to take shape.

2000–2007: Kazakhstan pulls ahead

From 2000 onward, the region’s economies began to follow very different trajectories. Kazakhstan entered its oil decade: GDP grew by 9.8% in 2000 and by 13.5% in 2001, a record that would not be surpassed over the next 25 years. The CPC pipeline began operating in 2001, Tengiz reached its design capacity, and oil prices were rising. Between 2000 and 2007, Kazakhstan’s GDP grew by around 10% a year on average. Over this period, Kazakhstan’s economy more than doubled in real terms. In nominal dollar terms, GDP increased more than fivefold, supported by rising oil revenues, inflation and a stronger tenge.

Uzbekistan grew steadily rather than in sharp jumps. At the beginning of the decade, growth was around 4–5% a year, before rising to 7–9% later in the decade. The economy remained closed, foreign investment inflows were minimal, but the strong role of the state helped preserve basic stability.

Turkmenistan was volatile: after 16.5% growth in 1999 following a new gas contract, growth fell to just 0.3% in 2002, before accelerating again to 13% by 2005. Tajikistan was recovering quickly from a very low base, growing by 8–11% annually, although GDP remained extremely small in absolute terms. Kyrgyzstan also grew, but its dynamics remained unstable. Kumtor boosted the economy when production was strong, while disruptions at the mine immediately led to slowdowns.

2008–2009: The first global shock to the region

The global financial crisis hit each economy differently. Kazakhstan saw a sharp slowdown: from 8.9% growth in 2007 to 3.3% in 2008 and 1.2% in 2009. Oil prices fell, and the banking sector, after the mortgage boom, was overloaded with debt. BTA Bank and Alliance Bank defaulted on external obligations. Together, these factors turned what began as an external shock into a systemic crisis.

The rest of the region came through the period with less damage. Uzbekistan maintained growth of 8.1% in 2009, as its closed economic model shielded it from financial turbulence. Turkmenistan grew by 6.1%, and in December 2009 launched its first pipeline to China, a structural turning point for the country’s entire gas export strategy. Tajikistan and Kyrgyzstan saw more moderate slowdowns.

2010–2014: Recovery and new risks

Kazakhstan recovered quickly after the crisis, growing by 7.3% in 2010 and 7.4% in 2011. Oil prices rose again, and Kashagan was preparing for launch. But after hydrogen sulfide leaks were discovered in 2013, the launch was delayed by a year and later postponed again, costing Kazakhstan billions in lost revenue.

Turkmenistan entered its golden period, growing by 9–15% almost every year from 2008 to 2014, except for 2009, when growth slowed to 6.1%. China was buying more gas, infrastructure was being built, and a new Ashgabat was rising. Between 2005 and 2014, GDP nearly tripled in real terms. Yet the structure of the economy barely changed: gas remained the main and effectively the only driver.

Uzbekistan held growth at around 7% in 2012–2014, supported by construction, textiles, and the automotive industry. Tajikistan maintained 7–8% growth on the back of the Rogun hydropower project and mining. Kyrgyzstan remained the most volatile economy in the region: growth reached 10.9% in 2013, when Kumtor was operating at full capacity, but the economy contracted during years of disruption at the mine — by 0.5% in 2010 and 0.1% in 2012.

2015–2016: The oil price crash

The impact of the late-2014 oil price collapse was felt in Central Asia with a delay. Kazakhstan grew by only 1.2% in 2015 and 1.1% in 2016. Formally, this was not a recession, but for an economy used to 7–9% growth, it felt like a standstill. The tenge was devalued twice, in February 2014 and August 2015, contributing to a decline in real incomes.

Uzbekistan’s growth slowed to 5.9% in 2016, its lowest rate in a decade. Turkmenistan’s growth eased to 6.2–6.5% as China began pressing down on gas prices. Tajikistan and Kyrgyzstan remained within the 4–7% range, and their lower dependence on commodities worked in their favor at that moment.

2016 also marked the beginning of a new stage for Uzbekistan: Karimov’s death in September opened the way for reforms.

2017–2019: Uzbekistan opens up

Under Mirziyoyev, Uzbekistan liberalized its exchange rate in 2017, opened the capital account, and launched privatization. Foreign investment began to enter the country. Growth started to accelerate. At first glance, 4.4% growth in 2017 may look modest, but that year became the first real point of recovery after the previous slowdown. The economy then accelerated to 5.6% and 6.8% in 2019.

Kazakhstan recovered to 4–4.5% growth in 2017–2019. Kashagan finally began operating steadily, but only after a 15-year delay and cost overruns that pushed the project several times over its initial budget. Turkmenistan slowed to 6–6.5% amid an internal energy crisis and chronic underinvestment in infrastructure. Kyrgyzstan and Tajikistan remained in the 4–7% range.

2020: COVID-19

In 2020, the region faced another major external shock. Kazakhstan contracted by 2.5%, its first recession since 1998. Kyrgyzstan contracted by 7.1%: tourism collapsed, Kumtor faced COVID-related restrictions, and remittances from Russia declined.

Tajikistan maintained positive growth at 4.4%, largely because the country imposed almost no lockdown restrictions. Uzbekistan’s growth slowed sharply to 1.6%, a clear break from the stronger growth rates of previous years. Still, the economy avoided recession. Turkmenistan recorded 5.9% growth, as its closed economy once again helped shield the country from the external shock.

2021–2024: The post-COVID recovery

The post-COVID recovery was uneven across Central Asia. Kazakhstan maintained moderate growth of 3–5% a year. The expansion of Tengiz and the operation of Kashagan supported the economy, while price volatility limited stronger acceleration. Kazakhstan’s GDP in 2024, according to WDI, reached around $291 billion, making it by far the largest economy in Central Asia.

Uzbekistan accelerated: 8% in 2021, 6% in 2022, 6.3% in 2023, and 6.5% in 2024. The country’s GDP reached $114 billion in 2024. It remains below Kazakhstan’s GDP, but the gap is gradually narrowing. One of the key growth factors is gold: gold exports amount to 6.6% of GDP, and the global rally brought the country additional billions.

Tajikistan has shown the fastest growth in the region in recent years, expanding by 8–9.4% annually since 2021. The Rogun hydropower plant is still under construction, while industrial production is growing by 20% a year. But the base remains extremely low: GDP per capita is around $1,341 in 2024, so even high growth rates are only gradually narrowing the gap with neighboring countries.

Kyrgyzstan unexpectedly accelerated to 9% growth in 2022–2024. After 2022, the country became a transit hub for parallel imports to Russia, and trade, together with the financial sector, gave the economy a sharp boost.

Turkmenistan continues to report official growth of 6–6.3%, but the quality of the data raises questions. The country does not publish detailed statistics, forcing international organizations to rely on official figures.

The 30-year outcome

Over 30 years, Kazakhstan has built the region’s largest economy, largely driven by oil revenues. The country is now looking for ways to reduce its reliance on oil as the main source of growth. GDP per capita remains higher than in Uzbekistan, but the structure of the economy is still strongly tied to commodities.

Over the past decade, Uzbekistan has emerged as one of Central Asia’s strongest growth performers. Reforms are working, foreign investment is coming in, and industry is diversifying. Kazakhstan will remain ahead in absolute GDP for a long time, but Uzbekistan has been growing faster for several years in a row.

Tajikistan is industrializing and building energy independence. Once completed, the Rogun hydropower plant will double electricity production and could turn the country into a regional energy exporter. This has the potential to fundamentally change Tajikistan’s economic model.

Latest news

Our latest stories in focus.